The holiday season has begun and parents are asking how to start buying stocks for the children in their lives. Here are a few options from simple and easy to a bit more complicated.

If there’s a child, or children, in your life that you’d like to purchase shares of stock for, here are a few options to make it happen:

Gift a Share

The easiest way to gift a single share of stock to a child, or anyone, is to visit a site like GiveAShare.com or UniqueStockGift.com and purchase a share of stock just like you would purchase anything else online.

Pros

There are only a few choices so you won’t be overwhelmed with options.

You check out just like any other purchase so it’s quick.

After you pay, the website will mail a physical paper to the recipient. You can make it as nice or as plain as you’d like.

The company you purchased stock in will contact the recipient to get their tax payer information so you don’t have to be involved with social security numbers.

Cons

It’s expensive. The company is a middle person. A stock that’s trading for $7 may still have a “transfer fee” of$40 to $70.

The recipient will not receive an actual stock certificate. Most companies don’t offer them anymore.

Open an UGMA Account

Uniform Gift to Minors Act and Uniform Transfer to Minors Act (UGMA/UTMA) are investment accounts that require an adult open the account with the child. It will be technically be the adult’s account until the child comes of age. That age can range anywhere between 18 and 25 depending on your state. You can buy and sell stocks in these accounts at whatever amount the stock is trading at and you’ll pay minimal account fees (compared to gifting a share directly) however you’ll also have to manage an account.

Pros

It’s cheaper to purchase stock. So investments can gain value quicker.

You’ll be able to purchase more shares with the same amount of money since there will be fewer fees.

The child isn’t in control of the account (as long as you don’t give them the log in information) so you don’t have to worry about them making mistakes.

Cons

Someone will have to co-own the account with the child. That means someone will have to open the account with the child and adult’s social security numbers. If you aren’t the parent, asking for the child’s social may be a huge ask.

Whoever is on the account with the child is going to pay taxes on gains and must file taxes appropriately every year.

Open a Brokerage Account

Some investment firms will let teens open an investment account alone. These accounts have a few restrictions but generally function like any other investment account. If the child you want to gift stock to is at least 13 years old, this may be a good option. Check out Feidelity’s Youth Account.

Pros

The accounts often have financial education tools built right in so students can learn investing principles.

Some accounts allow fractional investing so you can provide a specific amount of money and the young person can choose how they’d like to purchase shares.

Since the account needs no co-owner, little personal information has to be shared.

Cons

Since there is no adult co-owner it may be difficult to monitor the young person’s choices.

Suggestions

If you are a parent, opening up a UGMA or UTMA account for a young child makes the most sense. If you’re a parent but your child is a teenager, opening up a youth brokerage account might make more sense.

If you are an auntie, cousin, padrino, etc. then gifting a share of stock is easier and requires fewer entanglements.

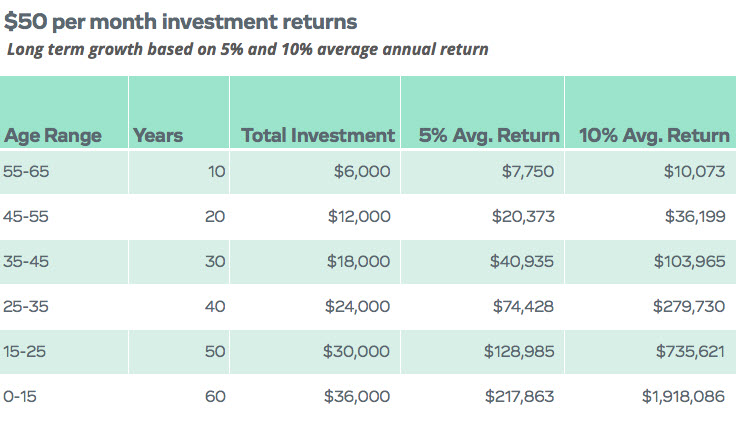

Regardless of how you choose to introduce stocks to the young people in your life, there’s no time like now to get started. The one thing that young people have in their favor is time. Even if you can only provide $20 per month (or $240 a year), that $20 could grow to $97,000 assuming you provide $20 per month for ten years and got a 7% annual return and then NEVER PUT ANOTHER DOLLAR IN. Imagine if you started with $20 per month when they were ten years old and then your young person added $50 once they began working … and then they increased that contribution to $100 once they got a full-time job … and then … well, you get the picture.

In case you want to play with the numbers, check out this compound interest calculator.

Happy buying assets instead of liabilities this holiday season!

Shay Olivarria is the most dynamic financial education speaker working today. Previous clients include: Gateway Technical & Community College, SCE Credit Union, American Airlines Credit Union, and San Diego City Community College, among others. She has written three books on personal finance, including Amazon Best Seller “Money Matters: The Get It Done in 1 Minute Workbook”. Shay has been quoted on Bankrate.com, FoxBusiness.com, NBC Latino and The Credit Union Times.The 2nd edition of “10 Things College Students Need to Know About Money” is available now.

For all of my personal finance tips, order my book “

For all of my personal finance tips, order my book “

hay Olivarria is the most dynamic financial education speaker working today. Previous clients include: Gateway Technical & Community College, SCE Credit Union, American Airlines Credit Union, and San Diego City Community College, among others. She has written three books on personal finance, including Amazon Best Seller “Money Matters: The Get It Done in 1 Minute Workbook”. Shay has been quoted on Bankrate.com, FoxBusiness.com, NBC Latino and The Credit Union Times.The 2nd edition of “

hay Olivarria is the most dynamic financial education speaker working today. Previous clients include: Gateway Technical & Community College, SCE Credit Union, American Airlines Credit Union, and San Diego City Community College, among others. She has written three books on personal finance, including Amazon Best Seller “Money Matters: The Get It Done in 1 Minute Workbook”. Shay has been quoted on Bankrate.com, FoxBusiness.com, NBC Latino and The Credit Union Times.The 2nd edition of “

hay Olivarria is the most dynamic financial education speaker working today. Previous clients include: Gateway Technical & Community College, SCE Credit Union, American Airlines Credit Union, and San Diego City Community College, among others. She has written three books on personal finance, including Amazon Best Seller “Money Matters: The Get It Done in 1 Minute Workbook”. Shay has been quoted on Bankrate.com, FoxBusiness.com, NBC Latino and The Credit Union Times.The 2nd edition of “

hay Olivarria is the most dynamic financial education speaker working today. Previous clients include: Gateway Technical & Community College, SCE Credit Union, American Airlines Credit Union, and San Diego City Community College, among others. She has written three books on personal finance, including Amazon Best Seller “Money Matters: The Get It Done in 1 Minute Workbook”. Shay has been quoted on Bankrate.com, FoxBusiness.com, NBC Latino and The Credit Union Times.The 2nd edition of “

If you’re like me, you want to use your money well. You want to buy things you want. You want to pay yourself first by setting a few dollars aside for emergencies and investing a few coins for retirement. You want to pay your bills on time, and in full every month but those things rarely happen the way you know they should. Behavioral economics explains that most people do better when things are automated and we don’t have to actively make choices. Why do you think so many people know exactly what they need to do and then they still don’t do it?

If you’re like me, you want to use your money well. You want to buy things you want. You want to pay yourself first by setting a few dollars aside for emergencies and investing a few coins for retirement. You want to pay your bills on time, and in full every month but those things rarely happen the way you know they should. Behavioral economics explains that most people do better when things are automated and we don’t have to actively make choices. Why do you think so many people know exactly what they need to do and then they still don’t do it?